The SEC’s Division of Economic and Risk Analysis (DERA) recently released its analysis of custom tag usage in financial filings submitted to the SEC using the US GAAP financial reporting taxonomy. This analysis focuses on XBRL exhibits submitted by issuers complying with the 2009 Interactive Data rules pertaining to financial statements. The study covered exhibits submitted as part of Forms 10-K and 10-K/A filings from January 2017 to December 2019.

Wednesday, July 22. 2020

US GAAP Trend Analysis 2019

As per SEC rules concerning XBRL submissions, filers may create custom XBRL tags when the standard taxonomy does not provide a tag for the necessary financial element. This customization accommodates unique circumstances in a filer’s particular disclosure. However, as a consequence, the use of unnecessary customized tags could potentially reduce the comparability of inter-company data. Therefore, the SEC’s rules specify the circumstances under which a filer may create custom tags.

|

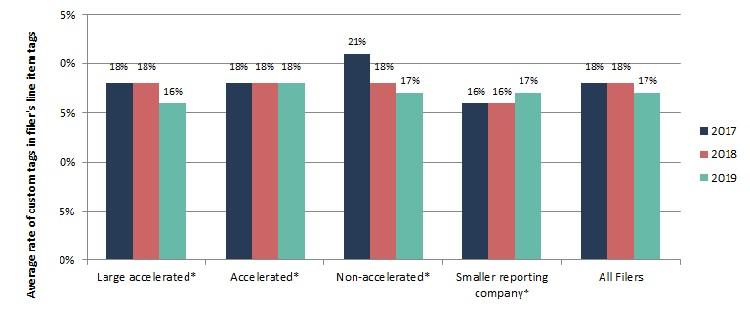

Custom tag usage in Forms 10-K and 10-K/A from 2017 to 2019 separated by self-identified filer category. Source: sec.gov.

When considering the breakdown of filers, DERA staff identified “large accelerated filers,” “accelerated filers,” “non-accelerated filers,” and “smaller reporting companies” using the filers’ self-identifications in the XBRL data of their Forms 10-K and 10-K/A. Note that the SEC adopted amendments to the definition of “smaller reporting company” on June 10, 2018 with the rule effective date of September 10, 2018. The SEC also modified several forms (including Form 10-K) and directed filers to check all applicable boxes on the cover page addressing accelerated and large accelerated filer status, SRC status, and emerging growth company status.

For the purposes of this analysis, DERA included filers that self-identified as smaller reporting companies and also reported a separate filer status (i.e., large accelerated filer, accelerated filer, or non-accelerated filer status) in the respective categories of large accelerated filers, accelerated filers, or non-accelerated filers. Also included were other filers that only reported one filer status (i.e., large accelerated filer, accelerated filer or non-accelerated filer). Given the cover page modification and the consequent increase in filers self-identifying as smaller reporting companies while also reporting a separate filer status, such companies were included in the smaller reporting company category for 2019 in order to maintain the trend analysis on smaller reporting companies. In addition, the smaller reporting company category contains twenty filers that self-identified as smaller reporting companies and did not report a separate filer status in 2019. DERA did not verify the accuracy of the filers’ self-identification as doing so was beyond the scope of the present analysis.

The trend analysis for Forms 10-K and 10-K/A indicated that the average custom tag rate usage for the filers generally remained constant from 2017 to 2018 but decreased in 2019. Custom tag rates for large accelerated filers and non-accelerated filers declined over the three-year assessment period, while custom tag rates for accelerated filers remained flat. Custom tag rates for smaller reporting companies stayed constant from 2017 to 2018 but increased in 2019.

DERA staff will continue reviewing filers’ use of XBRL custom tags in their submissions to the SEC. DERA may share additional trends, issue guidance, or pursue other actions, depending on the results of their analyses. See this website for the staff observations DERA staff published on custom tag rates in 2014. For DERA’s previous trend analyses on custom tags, see the Trends section on this page. DERA welcomes questions and comments. Interested parties can contact the Division at (202) 551-5494 or through email at StructuredData@sec.gov.

Sources: